The May USO trade did not work.

That is the simple version. It is also the incomplete one.

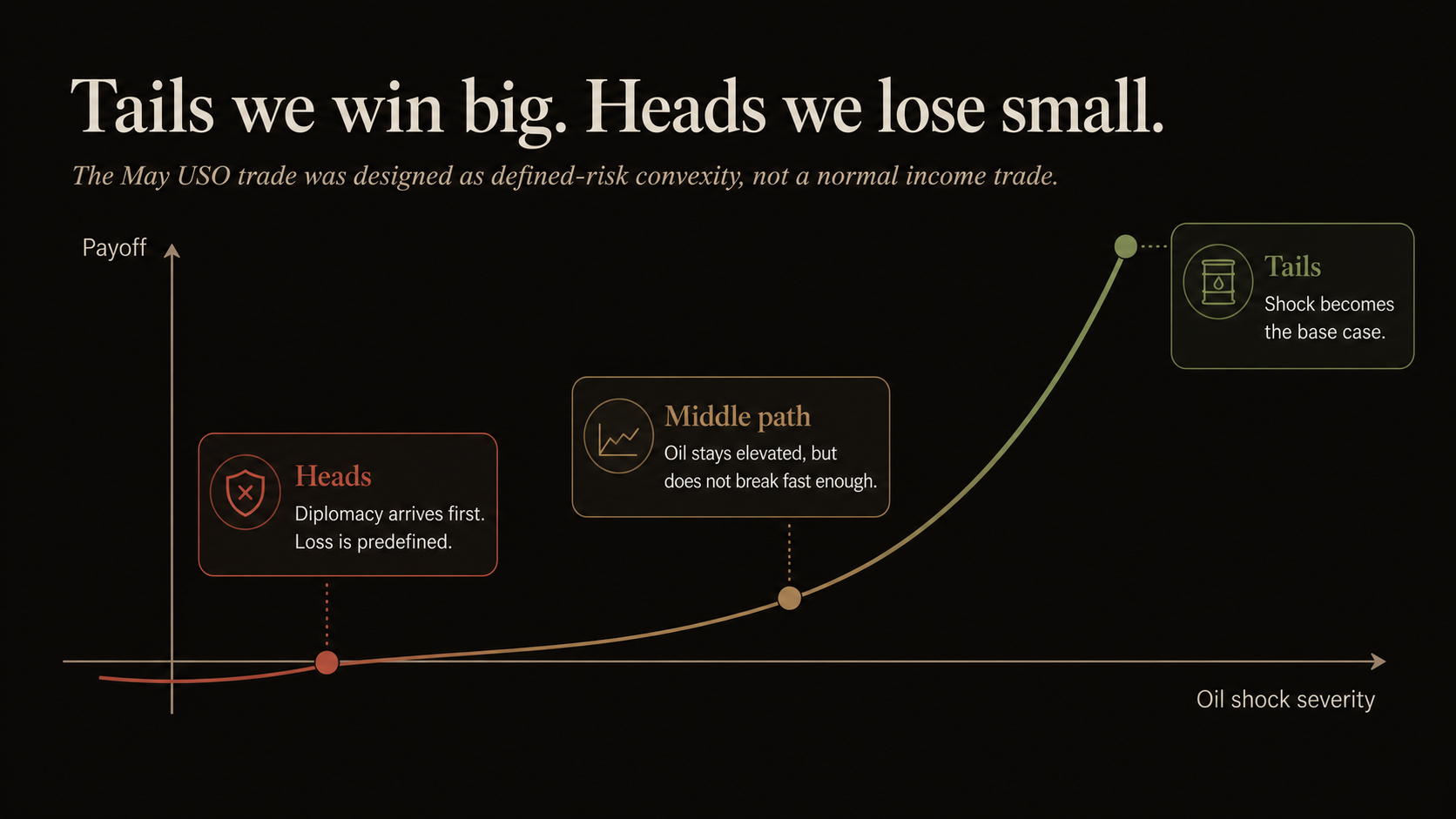

The trade was built as a defined-risk oil shock position. If the Strait of Hormuz stayed closed, shipping remained frozen, and the market was forced to price physical scarcity before May expiration, the payoff could be several times the premium at risk. If diplomacy arrived first, or the oil squeeze faded, the loss was known from the beginning.

That was the bargain: tails we win big, heads we lose small.

I still think that was the right kind of bet to make. The structure was asymmetric, uncorrelated to the rest of the book, and tied to a real physical-market stress. It was not a normal Workflow Capital trade. We are put sellers. We collect volatility premium on companies we want to own. This was different. It was a macro option on disorder in the oil market.

Sometimes those pay. Sometimes they expire. The discipline is not pretending otherwise.

What Changed

The catalyst changed before the clock ran out.

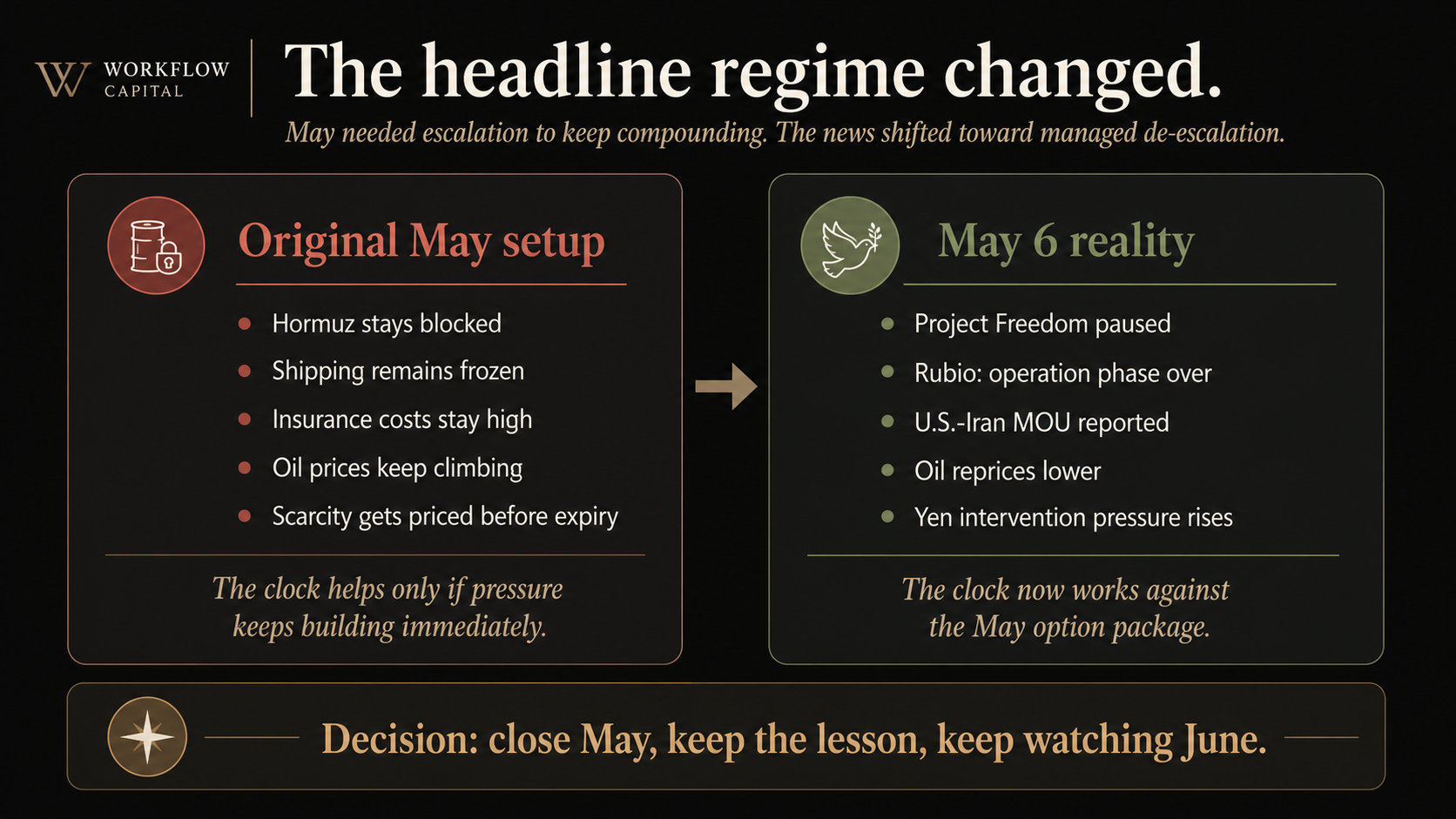

The original May thesis needed pressure to keep building into expiration. Hormuz had to stay blocked. Insurance had to stay expensive. Shipping had to remain frozen. Oil had to keep moving higher.

For a few weeks, that path was alive. USO traded into the high $140s, and the position had windows where it was profitable.

Then the headline regime changed.

Trump paused Project Freedom, the U.S. effort to escort stranded vessels through the Strait of Hormuz, so negotiations with Iran could continue. Marco Rubio said the major U.S. operation phase was over. Reporting from Axios described a possible one-page framework between the U.S. and Iran that would start a 30-day negotiation period, reopen Hormuz gradually, limit Iran's nuclear program, and ease sanctions in stages.

None of that meant peace was guaranteed. It did mean the market no longer had to price only escalation.

Oil responded immediately. USO fell back into the low-to-mid $130s. WTI moved back into the mid-$90s. The May options still had value, but the path to a large payout had narrowed sharply.

With nine days left, we were no longer being paid to wait.

The Yen Was a Tell

The currency market gave the same message.

Japan had likely spent around $35 billion buying yen, based on Bank of Japan account data reported by Reuters. The yen had been under pressure because Japan imports its energy. High oil and a weak yen are a bad combination: higher import costs, higher inflation pressure, and more political stress.

That matters for an oil trade.

When the Bank of Japan and Ministry of Finance are leaning against yen weakness, and the U.S. is leaning toward a Hormuz settlement, and oil is falling on deal optimism, the system is telling you something. Policymakers are no longer passively accepting the oil shock. They are trying to damp it.

That does not kill the long-term oil thesis. It does change the odds for a nine-day option.

Why We Closed May

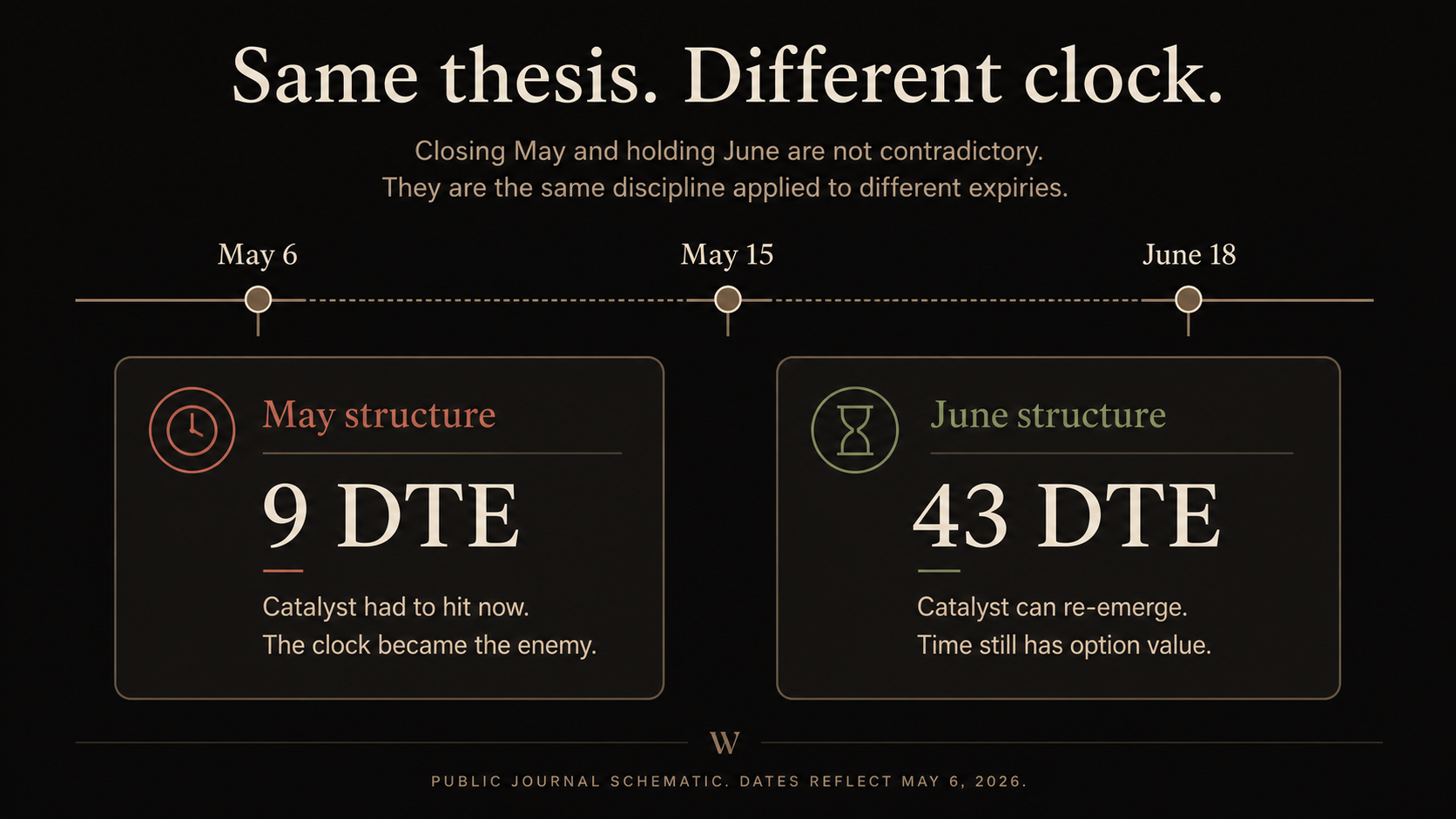

By May 6, the May structure had become too dependent on an immediate reversal in the news.

Could diplomacy fail? Yes.

Could Iran fracture internally and the conflict restart? Yes.

Could oil spike again? Absolutely.

But the May position needed that to happen almost immediately. The expiration clock had become the enemy. The trade was no longer "own cheap convexity on an oil shock." It was "hope the diplomatic headline reverses before time value disappears."

That is a different trade.

So we closed the May structure and took the loss. Not because the original idea was wrong. Because the remaining version of the idea was no longer attractive.

What Remains

The June structure remains different.

June still has time. A deal can stall. Implementation can fail. Shipping can remain slow. Insurance can stay restrictive. Political factions inside Iran can reject the settlement path. The market can move back from relief to doubt.

May needed the catalyst now. June still owns the possibility that the catalyst returns later.

That is why closing May and holding June are not contradictory. They are the same discipline applied to two different clocks.

The Lesson

The painful lesson is not that we took the trade.

The painful lesson is that we did not reduce it when the market gave us the chance.

When USO was in the high $140s, the May structure had done enough to deserve a partial exit. The thesis was still alive, but the expiration clock was short. That is exactly when an asymmetric trade should be harvested in pieces.

We did not do that. We waited for the full thesis.

That was the mistake.

For future event-driven convexity trades, the rule should be clearer:

- Define the headline that invalidates the clock, not just the price target.

- If the position doubles with less than two weeks to expiry, take partial profits.

- Treat diplomacy as a volatility-crush catalyst.

- Once a far-out-of-the-money option needs an extreme move inside ten days, it is no longer a lottery ticket. It is salvage value.

This was a small loss by design. That is the point of the structure. Heads we lose small.

The job now is to keep the lesson and not confuse a defined loss with a bad process.

Sources Checked

- Guardian, May 6: Trump paused Project Freedom to pursue an Iran deal; Rubio said the operation phase was over and Hormuz reopening was now part of the demand set.

- Axios, May 6: U.S. and Iran close to one-page MOU framework for ending war, opening Hormuz negotiations, limiting enrichment, and easing sanctions.

- Reuters/Investing.com, May 6: Dollar fell against yen as intervention chatter swirled and optimism grew for U.S.-Iran deal; WTI futures down sharply.

- Reuters/Investing.com, May 1: BOJ data suggested Japan may have spent roughly $35 billion on yen-buying intervention to support the currency.

Carlos Taborda Jaraba

Founder & Portfolio Manager

Workflow Capital